A central thesis of Marx is that the rate of profit is the major influence on the level of investment. In Capital Vol. 1, throughout the chapters on the accumulation of capital it is implicit that it is competition which is driving accumulation. The profitability achieved by a firm is the decisive test of its competitive success or failure. Profits provide the key source of capital to finance increases in investment and accumulation.

However Marx does not see profits as determining investment in a process of mechanical causation. He recognises that decisions about the allocation of capital take place in real time, and are made by capitalists who are making choices about their investment strategies while facing an uncertain future. It is essential in political economy to acknowledge this moment of agency, otherwise we elide the dimension of risk in capitalist calculation and outcomes.

But of course, Marx is not an methodological individualist. The investment decisions which capitalists take are subject to the selective processes implemented by the law of value. This term summarises all the ways in which the competitive failure or success of companies are determined by how economically and efficiently they make use of the labour and means of production at their disposal. And also by the balance of supply and demand in the markets in which they buy and sell.

Thus the choices of individual capitalists are subject to the discipines of technological and market competition. For example Marx documents in detail how the spread of steel spindles in textile production lowered costs of production. He sardonically notes that the capitalist does not have to use spindles made of steel just because his competitors do. But the price he gets for the product will be determined by steel spindle technology, if that has come into general use.

If the capitalist has a foible for using golden spindles instead of steel ones, the only value which counts for anything in the value of the yarn produced remains that which would be required to produce a steel spindle, because no more is necessary under the given social conditions [i.e. current technology]. (Capital Vol. 1, p. 295).

How much to invest and in what? These decisions are made in a situation of uncertainty. The laws of competition are coercive, but they are not automatic and entirely predictable.

Marx did not see a simple linear relationship of cause and effect between profit and accumulation. Note, for example, his comment on a book by the Rev Richard Jones whom Marx considered to be less stupid than the other prominent parson economists of the period, Malthus and Chalmers. ‘Jones is right to stress that despite the falling rate of profit, the “inducements and faculties to accumulate” increase’ (Capital Vol. 3, p. 375). Here Marx quotes and endorses the comment by Jones that:

A low rate of profit is ordinarily accompanied by a rapid rate of accumulation, relatively to the numbers of the people, as in England … a high rate of profit by a lower rate of accumulation, relatively to the numbers of the people. Examples: Poland, Russia, India etc.

Marx emphasises that capitalists are conflicted about whether to reinvest their profits in the expansion of production, or use them to finance speculative ventures. Here again Marx stresses the moment of agency: ‘the individual capitalist … has the choice between lending his capitalist out as interest-bearing capital or valorising it himself as productive capital’ (Capital Vol. 3, p. 501, Penguin edition).

Profits can be used in luxury consumption, or to play the financial markets.

the progress of capital production not only creates a world of delights; it lays open, in the form of speculation and the credit system, a thousand sources of sudden enrichment (Capital vol. 1, p. 741).

The investment versus capitalist consumption dilemma was an important theme in the literature of political economy. In the early phase of classical political economy, capitalists were urged to reinvest as much as possible. In Marx’s concise summary, the message of Malthus and his contemporaries was as follows:

Accumulate, accumulate! That is Moses and the prophets … therefore save, save, i.e. reconvert the greatest possible portion of surplus-value or surplus product into capital! Accumulation for the sake of accumulation, production for the sake of production was the formula in which classical economics expressed the historical mission of the bourgeoisie in the period of its domination (p.742).

Marx notes, for example, that Thomas Malthus, recognised ‘the awful conflict between the desire for enjoyment and the desire for self-enrichment’. Marx agrees with this: he notes that surplus value is divided into two parts: (1) revenue – used to meet the consumption needs of capitalists and their families, (2) capital – for accumulation by reinvestment. (Capital Vol. 1 738-746). The capitalist, says Marx, experiences all the agonies of a Faustian conflict between the passion for accumulation and the desire for enjoyment (p. 741). (See Goethe’s Faust, lines 1112-3 – ‘Two souls, alas, do dwell within my breast; each seeks to sever from the other’. Faust is torn between the pleasures of the world and his longing to devote his life to the accumulation of knowledge and spiritual or magical power.)

Malthus’s solution to this dilemma was to advocate a division of social labour. He urged the capitalist class to live modestly and leave extravagant spending to other social groups – the landed aristocracy, the holders of sinecures, and the clergy.

But, after the 1832 July Revolution in France, and faced with a rising tide of industrial and social unrest in England, political economy altered course and began to celebrate not the acquisitive drive to accumulate of the entrepreneurial class – but rather the nobility and high moral mission of the capitalists.

As classical political economy degenerated into mere ideology, Marx notes for example how Nassau Senior begins to praise the self-sacrifice of the capitalist who, by his abstinence from consuming all of the surplus-value and surplus product, sacrifices his own consumption in order to provide workers with the machines and raw materials which they need for employment and wages. In Marx’s summary:

The capitalist robs himself whenever he ‘lends (!) the instrument of production to the worker’, in other words, whenever he valorises their value as capital by incorporating labour-power into them instead of eating them up, steam-engines, cotton, railways, manure horses and all (Capital Vol. 1, p. 745).

Surely, Marx continues, the simple dictates of humanity would enjoin the release of ‘that peculiar saint, that knight of the woeful countenance, the abstaining capitalist from his temptation and his martyrdom’ (p.746). (The knight of course is Don Quixotte – allusions to Cervantes’ novel are frequent in Marx’s writings). And here Marx notes a new and happy development which has brought relief to one particular group of self-sacrificing capitalists.

The slave owners of Georgia U.S.A. have recently been delivered by the abolition of slavery from the painful dilemma over whether they should squander the surplus product extracted by means of the whip from their Negro slaves entirely in champagne, or whether they should reconvert part of it into more Negroes and more land’ (Capital Vol. 1, p.745).

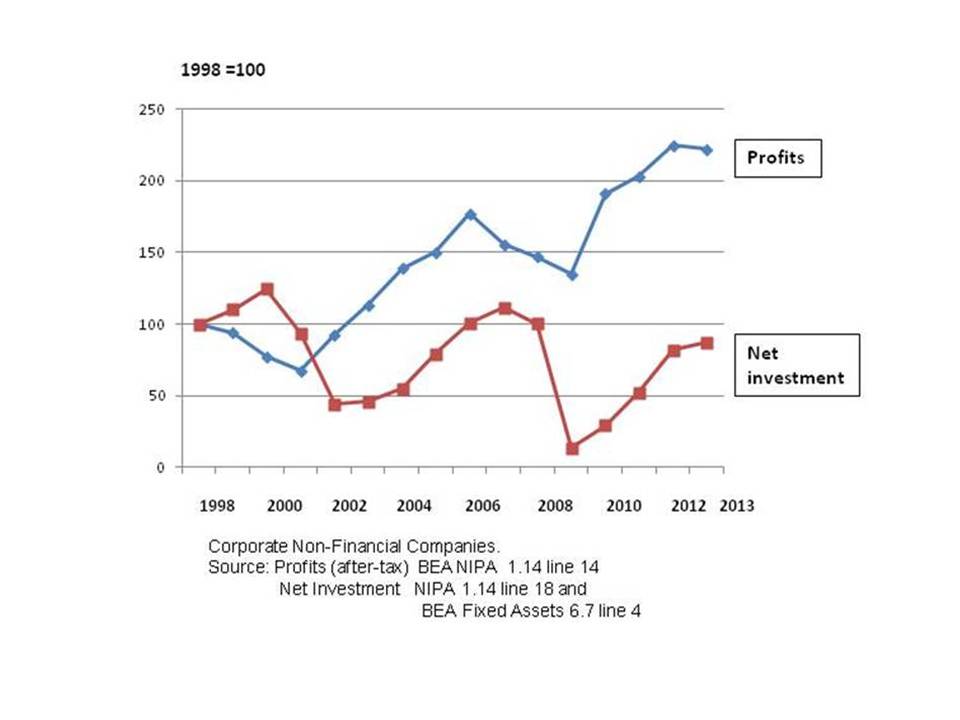

Consume or invest. The capitalist dilemma remains as prevalent today as in Marx’s period. The evidence is overwhelming that in recent years, in the high-income economies, consumption by the owners and controllers of capital has been winning out over accumulation. As investment has lagged, an increasing proportion of the rise in the mass of profit since 2000 has been handed out to shareholders in dividends and share buy-backs, or used to pay large increases in executive salaries.